Clint Ballinger

Austerity in a Time of Plenty: : The “domestic default” bogeyman = More bad statistics from Reinhart & Rogoff

The eminent Robert Skidelsky identifies three groups of economists who gave what ex post was clearly bad advice, and bad advice that mattered about fiscal policy, from 2009 on: Alberto Alesina and company with their “expansionary austerity” doctrines, Ken Rogoff and company with their “short-term-pain-for-long-run-gain” doctrines, and Ricardo Haussman and company with the “no choice but austerity” doctrines. All three groups, however, had reasons for their arguments and were thinking hard—albeit, in my view, not as hard and as deeply as they ought to have and had a responsibility to do—and genuinely believed what they were putting forward. There were also three groups of economists giving bad advice who either did not believe what they were saying or had done no thinking at all: Robert Lucas and company with his “nothing to apply a multiplier to” ideological and unfounded claims that fiscal policy could never be effective; John Taylor, Marvin Goodfriend, and company with their Bernanke’s monetary expansion will produce currency debasement and inflation but will not boost employment; and a whole host of professional Republicans who ought to have been backing up Bernanke’s plans for further monetary stimulus and his call for an end to fiscal austerity headwinds, but were instead very quiet, as Elmer Fudd would say, in part at least not to annoy political masters in the Republican Party. I think the economics profession could have played a useful role in helping to manage the recovery if those three groups unmentioned by Skidelsky had not been present....WCEG — The Equitablog

The very sharp Ken Rogoff predicts a boom over the next four years: "The biggest missing piece... is business investment, and if it starts kicking in... output and productivity could begin to rise very sharply.... You don’t have to be a nice guy to get the economy going.... It is far more likely that after years of slow recovery, the US economy might at last be ready to move significantly faster..."

I really can't see it as likely.Grasping Reality

Fatas says Rogoff "argues that the world economy is suffering from a debt hangover rather than deficient demand." I had to check that. When I read Fatas, I thought he might be misinterpreting Rogoff. He's not. He's right. Rogoff sees secular stagnation as one possibility, and crushing debt as "another possibility".

Rogoff sees the excessive debt explanation as an alternative to the deficient demand explanation.

That's just plain silly. Excessive debt is not an alternative to the "deficient demand" explanation. Excessive debt is the cause of deficient demand. First, the growing cost of growing debt consumes a growing portion of income. So demand atrophies gradually at first. Then, people suddenly come to think of their debt as excessive, and they suddenly cut their borrowing and spending. Demand falls suddenly -- economists call that a "shock" -- and we have "deficient demand".

In a very readable and insightful review of the new Martin Wolf book (which I haven’t read yet) Kenneth Rogoff plays the revolutionary card:’Let’s get rid of these debts, we’ve got nothing to lose than a deflationary chain of events’. This puts him, in a Eurozone perspective, in the radical left corner of politics (and it’s kind of ironic that he accuses text-book economists like Krugman of being ´hard-left´…).Real-World Economics Review Blog

And people really believe Harvard stands at the pinnacle of the intellectual meritocracy in the United States?Occasional Links & Commentary

On April 19, just after I had written about how the key academic research used to bolster austerity policies was exposed by a 28-year-old grad student at U Mass, Amherst, I got a surprise in my email box.

In the email, Erskine Bowles and Alan Simpson giddily announced their new deficit-reduction plan, which includes, among other things, a recommendation to increase the eligibility age for Medicare. Their plan would reduce debt as a share of GDP below 70 percent by 2023 and, as the Washington Postreports, “seeks far less in new taxes than the original, and it seeks far more in savings from federal health programs for the elderly.”

What’s incredible is that over the last week, the study by Harvard economists Carmen Reinhart and Ken Rogoff that famously warned of the dangers of government debt has been proven to be riddled with errors and questionable methodology. To recap: R&R’s paper purported to show that countries with public debt in excess of 90 percent of gross domestic product suffered negative economic growth. Austerity hawks everywhere used it to justify cuts that have cost people jobs and vital services. The original spreadsheet used by R&R was obtained by a U Mass grad student, who found that in addition to the mistakes already noted by several economists, there was a coding error in their Excel spreadsheet that significantly changed the results of their study.

As New York Magazine’s Jon Chait has pointed out, that same discredited research has been used by Bowles and Simpson to formulate their deficit-reducing austerity plans.

Let’s take a look at some ugly chronology.....AlterNet

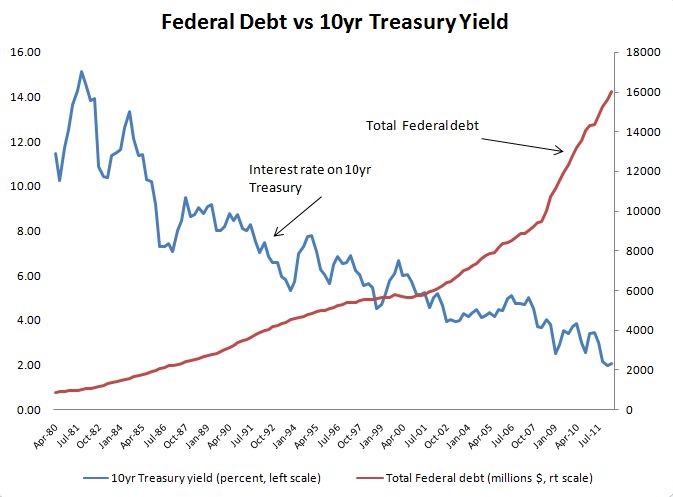

I love this chart so much I had to post it again. Here's the Federal debt (in red, millions $) and here is the rate on the 10yr Treasury (blue).

Hey Schiff, Rogers, Kotkikoff, Rogoff, Reinhart, Greenspan, Walker, Peterson, Simpson, Bowles, and the rest of you...what's your excuse now???