What about those "rules"?

This is potentially a big very deal going forward.

Russia Insider

Ukraine Prepares to Default on Its Russian Loan

Russia Insider

Ukraine Prepares to Default on Its Russian Loan

Alexander Mercouris

Most practically, the idea that the long-run "sustainability" of the debt requires efforts to control government borrowing -- an idea which goes unquestioned even at the far liberal-Keynesian end of the policy spectrum -- is a serious fetter on proposals for more stimulus in the short run, and is a convenient justification for all sorts of appalling ideas. And in general, I just reject the whole idea of responsibility. It's ideology in the strict sense -- treating the conditions of existence of the dominant class as if they were natural law. Keynes was right to see this tendency to view of all of life through a financial lens -- to see saving and accumulating as the highest goals in life, to think we should forego real goods to improve our financial position -- as "one of those semicriminal, semi-pathological propensities which one hands over with a shudder to the specialists in mental disease."The Slack Wire

On a methodological level, I see reframing the question of the evolution of debt in terms of the independent contributions of primary deficits, growth, inflation and interest rates as part of a larger effort to think about the economy in historical, dynamic terms, rather than in terms of equilibrium. But we'll save that thought for another time.

The important point is that, historically, changes in government borrowing have not been the main factor in the evolution of debt-GDP ratios. Acknowledging that fact should be the price of admission to any serious discussion of fiscal policy.

Please see the graph below that shows the breakdown of central government debt of 10 countries as a percentage of GDP. In the case of the United States, the figure used was debt held by the public. Intragovernmental debt (the debt the government owes to itself) was not included for obvious reasons. (It's ridiculous.)

So where are we, debt-wise? Pretty far down on the list.

Who has the highest debt-to-GDP ratio? Japan. They also have the lowest interest rates and just so you know...it's not because they "save" more or any other crap like that. It's because the Bank of Japan keeps their rates ultra-low in the belief that it will help the economy, which hasn't been the case for nearly 20 years. (They still don't get it.)

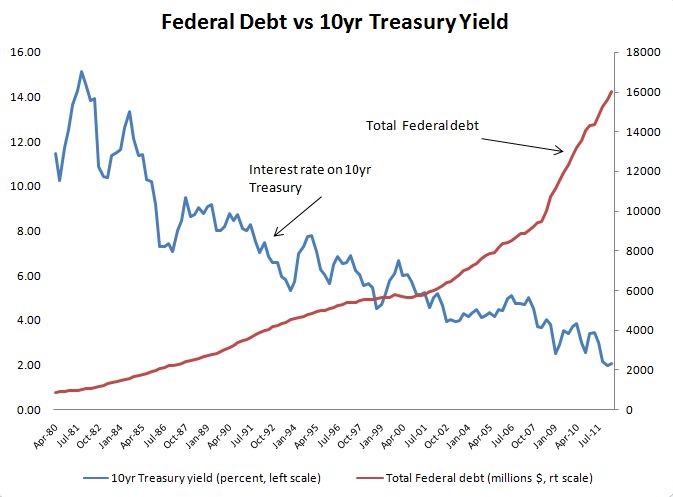

I love this chart so much I had to post it again. Here's the Federal debt (in red, millions $) and here is the rate on the 10yr Treasury (blue).

Hey Schiff, Rogers, Kotkikoff, Rogoff, Reinhart, Greenspan, Walker, Peterson, Simpson, Bowles, and the rest of you...what's your excuse now???

Read it at CNBC NetNet

Was the financial crisis caused by too little government debt?

We would add a few additional criticisms: • R&R did not distinguish between sovereign (debt issued in domestic, inconvertible currency) and non-sovereign (debt issued in, or pegged to, external or other forms of hard currency) governments. • Prevailing macroeconomic models still do not account explicitly for the fact that under a soft currency system, government deficit spending and debt constitute private sector saving and net financial assets. • Finally, although Bob obtained much of his ammunition from an interview with Rogoff, R&R haven’t been completely innocent of letting the “90%” and similarly bad memes spin out of control.

What would happen if the US Federal Government stopped issuing bonds? By Binve Report July 08, 2011 – Comments (4) I have talked about this issue many times in some detail: -- The Matter of Deficits, Sovereign Default, and Modern Mon...... -- Follow Up: QE is not Inflationary, Thoughts on Risk Asset...... -- One of the smartest comments I have read yet regarding Qu...... -- Inflation and Asset Price Responses, and the (Non)Correla...... But I thought in this post I would highlight the point in the form of a question, so that the answer can be immediately ascertained. First thing to point out is that the issuance of US Federal Government bonds is a Congressional constraint, it is not an operational one. There is a history associated with this, which I delve into detail here and here. I will keep this post concise and leave the statement as a given. If you are unfamiliar with the history surrounding this, read the linked posts. US Government Bond issuance does not 'fund' US Government spending. US Government Tax collection does not 'fund' US Government spending. When the US Government wishes to spend (on DoD projects, Social Security payments, Government payroll, etc.) it simply spends. Specifically the US Treasury credits private sector bank accounts that exist at the Federal Reserve. It marks up numbers in a spreadsheet. The essence of what occurs is no more complicated than that. For a more detailed description, refer here (Read the whole thing, but especially the section 'Mechanics of Federal Spending') Currently there is a Congressional constraint that all US Federal Government spending be matched by bond sales (this is a holdover from a convertible currency standard, see above links). Additionally there is a further constraint that this 'debt' (which is a huge misnomer) be capped to some value (the 'debt ceiling'). Both of these constraints have no operational bearing nor curb the ability of the US Government via the US Treasury to credit private sector bank accounts. These are self-imposed constraints, not operational ones. Moreover, the US Federal Government is sovereign issuer of the US Dollar, and as such is monopoly supplier of the currency. It is the source of all US Dollars in existence. It must spend these Dollars into existence before the non-government sector can accumulate them (see links above for more details). It becomes self-evident that the US Federal Government can never not have US Dollars, since it is the sole issuer of the US Dollar. Equally meaningless is the notion that the US Federal government can 'save' US Dollars (that by spending less / saving today will give it the ability to spend more tomorrow). This would be true for all currency users (citizens, companies, US states, etc.), but this is absolutely false for the currency issuer. The US Federal Government is not a 'super-household' and never has to 'finance' its spending. There is no such thing as a US Federal Government Budget Constraint (GBC). So what do US Government bonds 'do'? (from here) They allow the Federal Reserve to maintain its target short term rate. Deposits within the banking system create reserves. A bank manager has a few options with what to do with those reserves, after using a portion of those reserves to ensure balances are cleared and other maintenance activities, and to maintain reserve requirements (and it is worth noting that many banking systems in other countries have no reserve requirements at all). They could let it sit in the vault as cash (earning no interest). They could keep it on account at the Federal Reserve (which relatively recently now earn a mere 25 bp, they earned 0 for a very long time before that). They could lend the reserves overnight (at an interest premium) on the interbank lending network to banks that require reserves to meet requirements. Or one of the few options beyond that is the purchase of US Government bonds. Reserves are not lent out. With the purchase of the bonds the banks are able to earn more interest in a very liquid asset (the US Treasury market is by far the biggest on the planet). This is how this manifests in the current system: The Federal Reserve has a mandate to maintain short term interest rates consistent with its policy goals. If the banking system has a system-wide deficit of reserves relative to requirements, then competition overnight on the interbank network will drive up the short term interest rate. The Fed reacts to this by buying US Treasury bonds on the open market and prints reserves (out of thin air) in exchange for those bonds. The result is a system wide increase in reserves and a system wide decrease in the amount of US Government bonds (an asset swap). This allows the Fed to put a cap on the short term interest rate relative to its policy goals. On the flip side, If the banking system has an excess amount of reserves relative to requirements, then competition overnight on the interbank network will drive down the short term interest rate. The Fed reacts to this by selling US Treasury bonds from its portfolio on the open market. The banks trade their reserves in exchange for the bonds. The result is a system wide decrease in reserves and a system wide increase in the amount of US Government bonds (again, nothing but an asset swap). Since the Fed is the entity that 'printed' those reserves to begin with, they disappear 'into the ether' when they are returned to the Fed's balance sheet. Here are the key points: 1 ) The US Federal Government spends (via the US Treasury) by crediting private sector bank accounts at the Federal Reserve 2) There is a Congressional constraint that all US Federal Government spending be matched by Government Bond sales 3) There is a 'debt ceiling' associated with the size of outstanding Government bonds 4) Both 2 and 3 are self-imposed constraints with historical origins and neither are an operational constraint to Federal Spending 5) The US Federal Government is monopoly issuer of the US Dollar, is the source of all Dollars, and can never 'not' have Dollars 6) From 5, the US Federal Government can never become 'insolvent' in terms of honoring US Dollar denominated obligations. The only way it cannot honor its Dollar denominated obligations is if it *willingly decides* not to pay them. This is another self-imposed constraint, not an operational one 7) Net Federal Government spending (spending in excess of taxation) creates net deposits which creates net reserves in the banking system. An increase in reserves pushes down the overnight lending rate. The Federal Reserve maintains control of its target overnight rate by selling US government bonds from its portfolio (via OMO) to ensure demand for reserves (the overnight interest rate) matches its target policy rate. When all these points are considered, it becomes obvious that the US Government bond market: a) Does not *fund* anything (It did under a convertible currency standard but does not under a fiat currency floating exchange rate standard) b) Provides the non government sector with interest income which the US Government will always be able to provide since it is monopoly issuer of the US Dollar c) Has relevance in the US Monetary System to facilitate liquidity management operations. That's it. So what would happen if the US Government stopped issuing bonds tomorrow? From the perspective of the US Federal Government being able to spend .... NOTHING. It would still credit private sector bank accounts at the Federal Reserve (move numbers in a spreadsheet) just like it does today. But it would stop doing the additional step of issuing bonds as it did the crediting. This would mean that reserves would build up in the banking system and competition for reserves would become very small, pushing the overnight rate to zero (just like it is right now with the current level of excess reserves). So basically nothing would happen that isn't already happening in the banking system. In fact, the US Government doesn't have to void all the current bonds. Just stop issuing new ones. The old ones will then expire at maturity and the whole US Government bond system will just gradually go away over the next 3 decades (however the average bond duration held by the non-government sector is something like 6 years so it would lose relevance much sooner in actuality). At sometime in the future, if the Federal Reserve wanted a non-zero Fed Funds Rate, it could just start paying a remuneration rate on all reserves held at the Fed. That would become the new interest rate floor, and the unnecessary song and dance of OMO could be avoided altogether. The Private sector would come up with some new benchmark (instead of the 10 year and 30 year US Treasury bonds) to price longer term loans (corporate loans, mortgages, etc.). When you follow this logic all the way through, you come to this very simple and inescapable conclusion: The US Federal Government does not need the US Federal Government Bond Market (Primary Dealers, Secondary Dealers, PIMCO, etc.) to provide it with funds, IT IS OTHER WAY AROUND!! All of these political stunts about not raising the debt ceiling are a literal waste of time. All of this analysis about US going the way of Greece (which is a currency *user* of the Euro, not a currency *issuer*) is a waste of time. We have real problems to talk about and to deal with (unemployment, competitiveness, education, etc.), and we are wasting a great amount of time and energy talking about a non-issue (the debt ceiling, possible US Government 'insolvency', US Bonds rates 'skyrocketing', etc.). I suggest we stop. |