Neoliberal Professor J.Bradford DeLong admits that deregulation of the financial sector during the 1990's was a bad idea.

An excerpt: "It may even be the case that we ought to return to the much more tightly regulated financial system of the first post-World War II generation. That system served the industrial core well, at least as far as we can tell from the macroeconomic aggregates. We know for certain that our more recent system has not".

It is amazing that the word 'may' is included in the above excerpt and not the word "should'.

Thursday, June 30, 2011

Bloomberg: Geithner Going?

Treasury Secretary Timothy F. Geithner has signaled to White House officials that he’s considering leaving the administration after PresidentBarack Obama reaches an agreement with Congress to raise the national debt limit, according to three people familiar with the matter.Geithner hasn’t made a final decision and won’t do so until the debt ceiling issue has been resolved, according to one of the people. All spoke on condition of anonymity to talk about private discussions.

That would be two down with Larry Summers gone.

UPDATE: Geithner denies the rumor.

UPDATE 2: Geithner waffles.

From a balance budget amendment to gold and silver coin

It's getting crazier out there.

Good news, gold bugs. In an effort to promote hard money as an alternative to paper dollars, three tea party senators—Jim DeMint (R-SC), Mike Lee (R-Utah), and Rand Paul (R-Ky.)—introduced legislation this week to exempt gold and silver coins from taxation....

...states that are looking to go back to gold face a few obstacles—namely, that there's no infrastructure to actually handle an infusion of gold currency. Carrying around a pouch of gold coins would be a burden (and vaguely Medieval), and so boosters tend to agree that for it really to take off, you'd need a centralized storage facility and then a debit-card-like transaction system, neither of which currently exist. And then there's the cost: gold and silver coins from the US Mint are the only coins that could be used as legal tender, and there's a significant markup on those in addition to the taxes. The Lee-Demint-Paul bill is attempting to tackle just one piece of the problem by making it less cost-prohibitive....

The truth about industrial production and tax rates

I'm sick of hearing all this B.S. dogma about keeping tax rates low to incentivize production. From 1945 - 1980, when top tax rates ranged from 91% to 71%, industrial production grew 225% in America.

Since Reagan through today, when top tax rates were brought down dramatically, industrial production grew 77%.

This thing about taxes is just a bunch of bull.

I am not for higher taxes; that's not what the economy needs right now, but seriously, it's just a B.S. argument.

Corruption Watch: What would it cost to buy Congress back and end corruption?

Charles Hugh Smith at Of Two Minds asks, How Much Would It Cost To Buy Congress Back From Special Interests?

He does the numbers and and estimates about 14 billion, with the president thrown in (veto power, you know).

When you think about how tiny $14 billion is compared to the $3.8 trillion Federal budget and the $14.5 trillion U.S. economy, it makes you want to weep; how cheaply we have sold our government, and how much we suffer under the whip of those who bought it for a pittance.

Corruption Watch: Sunny Sheu and now reporter Will Galison

Anyone that has been following Bill Black, Yves Smith, Janet Tavakoli, and others exposing corruption knows that it is endemic to the degree of becoming institutionalized and legalized, with very little push back and those who do push back face confrontation from powerful forces. This takes it to an new level, however — intimidation and murder.

Bill Gross Goes All In: "Who will buy them now?"

PIMCO bond "guru" Bill Gross has apparently re-tweeted his assertion that without the Fed buying US Treasury Bonds under QE2, no one will buy US Treasuries. (HT ZeroHedge)

Today is the last day for the Fed's open market operations known as "QE2", so Gross apparently took this opportunity to re-emphasize his current position that no one will buy Treasury bonds once the Fed stops.

Here's a link to his "tweet" and I quote: "Who will buy them now?" (Ed.: Unbelievable!)

Today is the last day for the Fed's open market operations known as "QE2", so Gross apparently took this opportunity to re-emphasize his current position that no one will buy Treasury bonds once the Fed stops.

Here's a link to his "tweet" and I quote: "Who will buy them now?" (Ed.: Unbelievable!)

I think bonds are actually going to rally once the Fed exits this marketplace, as they have been acting as a deep-pocketed scale-down buyer, in a market where there has been much speculative selling.

Wednesday, June 29, 2011

Fed extends dollar swap lines to foreign central banks--AGAIN!

Here's the article.

The Fed is at it again. This is like the fourth or fifth time in the past three years that the Fed has come to the rescue of foreign banking institutions and corporations. By instituting dollar swap lines the Fed provides dollar based liquidity to foreigners who are short dollars and need to make good on their dollar denominated obligations. In return the Fed assumes unlimited risk on this position.

The Fed doesn't have to do this. Central banks of these respective countries and trade zones could provide dollars buy selling their domestic currencies and buying dollars in the foreign exchange markets. But, heaven forbid, that would mean weakening their currencies and making the dollar stronger! So instead of doing that the Fed REMOVES that potentially huge dollar bid. And this comes from Bernanke, who recently talked about wanting a strong dollar??? Unbelievable.

Most shocking, however, is the fact that there is no outcry from Congress or any policymaker that has been complaining about the weakness of the buck. None whatsoever. Where are they?

Mish on age demographics

Mish provides a summary of recent reporting and concludes:

One of the many consequences of boomer demographics is the longer the US opus of reform of Medicare, and Social Security, the more difficult it will become because of voting demographics.

Republicans are already learning that from the negative reaction to the Ryan Plan — after they all signed onto it.

This is a plus from the MMT perpsective, since there is no reason to cut social services due to "affordability," when the only constraint is availability of real resources.

How to allocate real resources is a political decision, however, and the demographics suggest that the boomers will have the upper hand at the voting booth.

Some Democrats are floating the notion that the debt ceiling is unconstitutional

Catherine Rampell at The New York Times: Could Obama Just Ignore the Debt Ceiling?

Ryan Grim at The Huffington Post: 14th Amendment: Democratic Senators See Debt Ceiling As Unconstitutional

Beowulf has already told us some time ago that the Supreme Court decided that Congress does not have the authority to renege on obligations previously entered into on behalf of the United States. See Perry V. United States, 294 U. S. 330 (1935).

Case closed.

Now do the spineless Democrats have the spine to do this? That question answers itself.

Martin Wolf schools BIS on sectoral balances

Martin Wolf has an interesting post from the MMT perspective today in his column at The Financial Times.

Now turn to the yet more debated question of fiscal policy. The question I have is this: does the BIS know that every sector cannot run financial surpluses at the same time?Few doubt there is excessive private sector debt in a number of high-income countries. But how is it to be reduced? The BIS notes four answers: repayment; default; higher real incomes; and inflation. Let us rule out the last and focus on the first. Repayment means spending less than one’s income. That is what is happening in the US private sector (see chart). Households ran a financial deficit (an excess of spending over income) of 3.5 per cent of gross domestic product in the third quarter of 2005. This had shifted to a surplus of 3.3 per cent in the first quarter of 2011. The business sector is also running a modest surplus. Since the US has a current account deficit, the rest of the world is also, by definition, spending less than its income. Who is taking the opposite side? The answer is: the government. This is what a controlled depression means: every sector, other than the government, is seeking to strengthen its balance sheet at the same time.The BIS insists this is not good enough: highly leveraged countries are running structural fiscal deficits, which must be eliminated as soon as possible. Fair enough, but where are the offsetting adjustments to occur?

Read the whole post at Why austerity alone risks a disaster.

I posted a comment there commending him. Consider lending your support, too.

Tuesday, June 28, 2011

Euro MP Farage: "What is Plan 'B' For the Eurozone?"

Recent video from the RT of British MEP Nigel Farage on the current situation in the Eurozone. Evidence that at least some politicians in Europe have an independent, skeptical and objective view of the current situation and are asking some important questions.

Thought for the Day: The Pursuit of Happiness

What is the American Dream?: Dueling dualities in the American tradition by James Gustave Speth at New Deal 2.0 examines a key philosophical and normative fundamental that is central to the conception of economics, especially as it relates to policy formulation. It is worth a read in entirety. I intend to address these issues in future posts, since it involves the philosophical foundations of economics.

The American Dream is summarized in the Declaration:

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable rights, that among these are life, liberty and the pursuit of happiness. That to secure these rights, governments are instituted among men, deriving their just powers from the consent of the governed.

This is elaborated in the Constitution, and summarized in the Preamble:

We the People of the United States, in Order to form a more perfect Union, establish Justice, insure domestic Tranquility, provide for the common defence, promote the general Welfare, and secure the Blessings of Liberty to ourselves and our Posterity, do ordain and establish this Constitution for the United States of America.

It is evident that both national security and a legal system based on order and justice are prerequisites preserving life and liberty, and that a democratically elected government responsible to the people is required to ensure that the benefits of good government are extended to all.

But the meaning of "the pursuit of happiness" is less clear. Speth lays out the different visions of happiness that have shaped political interpretation of it.

This is key for macroeconomics, especially, since it deals with government as a key economic factor. Accordingly, the conception of the purpose of both life and government underlie the assumptions of a macroeconomic theory, since macroeconomists shape their theories with an eye to policy formulation. Economic theories and especially macroeconomic theories can be viewed as providing the rationale for policy proposals that are normative through and through, in spite of being disguised as being entirely positive, e.g., neoliberalism.

Therefore, economics presupposes views of metaphysics as the study of what is, epistemology as the study of what we can know about what is, ethics as the study of what we ought to do about what is, and aesthetics as the study of how we should feel about what is, in addition to using science as an empirical method of testable explanation of how things stand and change state, and what this may imply causally.

Without a critical approach to economics through the philosophy of economics as a method for clarification of assumptions and other aspects of thought and language that remain implicit, economic reasoning is not only unclear but can also be misleading.

For example, there is growing interest in examining the assumption that growth is an adequate criterion for economic progress when it may not be related to happiness. Happiness is an ambiguous concept, so it must be clarified first. On examination, Speth shows, growth as an economic criterion is based on a conception of happiness that well-defined in terms of the survival of the fittest. Therefore, "growth" as a criterion can be determined by GDP change, regardless of distribution. This is the neoliberal assumption that has become conventional wisdom.

The problem with this is that the US has the largest GDP globally, but it is the lowest in many key social indicators that involve happiness considered as "utility," i.e., relative material satisfaction. On many measures, the US is not the happiest nation on earth, "American exceptionalism" notwithstanding.

A key concept of Modern Monetary Theory is public purpose. Certainly, this must relate to the founding documents, and in particular to key statements from those documents cited above.

How then should MMT define itself wrt "the pursuit of happiness"?

The neoliberal view is that maximum utility is the criterion of action, presuming homo economicus to be a rational actor pursuing self-interest and capable of being modeled econometrically in terms of a representative agent. This is presumed to be self-evident, but it is contradicted by research in both cognitive and social science, as well as having been dismissed as actually irrational by thinkers for millennia because it overlooks the inherently social nature of human beings.

Maximum utility is based on methodological individualism. It is called "methodological" because the assumption of self-interest as the guiding principle of human motivation is a methodological presumption. However, this presumption is often if not generally presumed to be ground in ontological individualism, that is, that individualism is constitutive of human nature. Some economists leave this implicit, while others, especially the Austrian School, make it explicit.

Others claim that such presumptions ignore society as a complex web of relationship, involving interdependence in modern societies, and now global society. This is called "community," and it is the meaning of "fraternity," in the Enlightenment political ideal of "liberty, equality and fraternity." Now "fraternity" is called "solidarity in Europe.

Modern Monetary Theory based itself on a broader view of methodological individualism than neoliberalism or Austrian economics, in that it agrees that individuals are the elements in complex social system, and explanation must be ultimately grounded in causal mechanisms that stem from individual action. However, it accepts that other factors are at work in shaping individual decisions other than rational self-interest as generally conceived by methodological individualism that presumes ontological individualism. Ontological individualism is an oversimplification of human complexity.

According to MMT, the purpose of government is public purpose, that is to say, government is to serve the public interest rather than dominant private interest groups. The public interest is distributive. Economic happiness is only one aspect of human happiness and it involves prosperity.

Microeconomics is about prosperity of households and firms, whereas macroeconomics is concerned with the prosperity of entire societies and in the age of globalization, with global prosperity. At the macro level, prosperity is necessarily distributed. Public policy is about achieving this distribution through government pursuit of public purpose, which complements the pursuit of private purpose by individuals and interest groups, such as firms.

Monday, June 27, 2011

Dr. Housing Bubble Talks Minsky

We went from normal finance in housing (that is paying for the mortgage with current income), to speculative finance (where paying for the mortgage was based on cheap financing tools and projected incomes), to Ponzi financing where current income was unable to pay for even the servicing of debt.

This is Hyman Minsky's financial cycle.

The Ponzi financing era is over yet banks want to pretend that it will come back soon. For this reason we have an enormous pipeline of shadow inventory properties....

Housing in the U.S. has reached a debt spiral. No longer can people use Ponzi financing to service their debts....

The only factor I see causing home values to rise is higher household incomes. Do we see that? Here in California the underemployment rate is close to 23 percent....

Both parties currently stand to protect the wealthy financial class. Yet Americans are largely catching on to this fine tuned orchestra of financial swindling. This is why the “housing bailouts” have done very little in actually boosting home prices. They have boosted banking profits however....

The only answer is to clear the inventory and move on without protecting the “too big to fail” and their scare tactics....

The fear of course is of doom but ironically flooding the market with cheaper homes will actually bring in new buyers that actually can afford the properties with the new lower range of American incomes. This will also free up more disposable income to spend on other goods that keep the market moving. The ‘doom’ scenario is merely for the banks. We agree that banks are a necessity but more so like a utility, strictly regulated (for checks, savings, and regular retail banking). Investment banking can do what it likes but failures will fall completely on the shoulders of their banking enterprise. The commingling of these two functions, retail and investment banking has been disastrous for the typical hardworking family....

No matter how you slice it, the era of Ponzi finance is over.

Who could have guessed?

Relative to national economic trends, states that increased spending enjoyed on average:• 0.2 percentage point decrease in the unemployment rate• 1.4 percent increase in private employment• 0.5 percent real economic growth since the start of the recessionIn contrast, states that cut spending saw on average:• 1 percentage point increase in the unemployment rate• 2.1 percent loss of private employment• 2.9 percent real economic contraction relative to the national economic trend

Gold?? Ha!!! Treasuries outperforming the yellow metal!

How ironic! Most people who bought gold did so while at the same time saying that U.S. Treasury bonds were a bubble! (BTW...you didn't hear that on this blog!)

Look who's laughing now!!!

Treasuries are outperforming gold.

The chart below is spot gold divided by the 30-year Treasury price. Gold is tanking!

Sunday, June 26, 2011

Edward Harrison: Metrics for Growth

GDP is only one of five factors. The others are industrial production, employment, retail sales and personal income....

So when we get the GDP report next Friday, we might could (as my grandmother would say) see positive numbers for the change in GDP. Some people will be dancing in the street, proclaiming the recession is over. Hold the phone on that one though, because you’ll know that it doesn’t really mean anything until it is confirmed by the other four metrics that we should be watching.

The Tradeoff between MMT and Government

Robin Koerner, publisher of WatchingAmerica.com, addresses the balance budget amendment in light of MMT's warning about what it would entail economically.

The Huffington Post: A Balanced Budget Amendment Would Change Everything

It seems to me that Koerner presents the tradeoff pretty well. What he is saying is that most people calling for a balanced budget amendment don't realize that everything has consequences and they don't understand the political benefit that is supposed to result has an economic cost, even a serious one, in the tradeoff. He piece is about the political/economic tradeoff, and he things that the decision criteria should be normative. He sees it as a tradeoff between prosperity and tyranny and comes down against tyranny. That appeals to a lot of people both on the right and left in this culture of crony capitalism and corruption, in which the state is seen increasingly as predator.

He understands the basic points of MMT about the fiscal balance and then considers the tradeoff in terms of government power. This and his previous post show that he has at least taken the trouble to investigate MMT. That's a plus, since we are at least engaging on a playing field where our existence is being acknowledged. Moreover, he is objecting to MMT not on positive grounds, which he seems to have conceded, but on normative preference. That seems like an advance for MMT to me, rather than having to confront ill-informed blather.

The main objection of both left and right to MMT policy is that it gives politicians too much power in its attempt to offset saving desire with fiscal policy through the sectoral balance approach and functional finance. The right is concerned with politicians using fiscal power to bribe the rabble for votes, and the left is concerned with state capture as the wealthy and influential bribe politicians with contributions needed in increasingly expensive campaigns. Koerner makes clear that his concern is not economic as much as political. He cautions that there is a tradeoff between economic concerns and political concerns, and that a balanced budget amendment would have consequences that MMT warns about.

I don't that this can be shrugged off politically. This is why the work that Bill Black and Randy have been doing on the blogs is addressing corruption is so important, and why proposals for reform like Warren has put out are key to putting the MMT position across politically as well as economically. I have also brought up the input of Michael Hudson on economic rent, which MMT hasn't dealt with specifically as far as I can tell. But this is a good argument for progressive taxation that distinguishes productive and unproductive gains and taxes the unproductive. MMT does talk about targeted taxation, and this is what progressives are looking for to address inequality.

What do you think?

Soros Sour on the EMU

Soros reiterated his view in a panel discussion in Vienna that the euro had a basic flaw from the start in that the currency was not backed by political union or a joint treasury."The euro had no provision for correction. There was no arrangement for any country leaving the euro, which in the current circumstances is probably inevitable," he said.While he called survival of the European Union a "vital interest to all," he said the EU needed structural changes to halt a process of disintegration.

This has been the MMT view since the inception of the EMU.

Saturday, June 25, 2011

Latest 3 Months Fiscal Posture

March/April/May 2010:

Total Treasury Account Withdrawals: $2,858

Minus Treasury Redemptions: $1,693

Equals Net Treasury Withdrawals: $1,165

Total Treasury Account Deposits: $3,038

Minus Treasuries Issued: $2,240

Equals Net Treasury Account Deposits: $798

M/A/M 2010 Deficit: $367B for the quarter

March/April/May 2011:

Total Treasury Account Withdrawals: $2,954

Minus Treasury Redemptions: $1,812

Equals Net Treasury Account Withdrawals: $1,142

Total Treasury Account Deposits: $2,883

Minus Treasuries Issued: $2,005

Equals Net Treasury Account Deposits: $878

M/A/M 2011 Deficit: $264B for the quarter

So YoY for the 3 months ended May, the fiscal deficit has decreased by $103B (367B to 264B), due to a increase in deposits (either tax receipts, or perhaps the Fed refunding it's outsized "profits" due to QE to Treasury this year), as net withdrawals (spending) are actually down, nominal, by $22B, YoY for these same 3 months.

Total Treasury Account Withdrawals: $2,858

Minus Treasury Redemptions: $1,693

Equals Net Treasury Withdrawals: $1,165

Total Treasury Account Deposits: $3,038

Minus Treasuries Issued: $2,240

Equals Net Treasury Account Deposits: $798

M/A/M 2010 Deficit: $367B for the quarter

March/April/May 2011:

Total Treasury Account Withdrawals: $2,954

Minus Treasury Redemptions: $1,812

Equals Net Treasury Account Withdrawals: $1,142

Total Treasury Account Deposits: $2,883

Minus Treasuries Issued: $2,005

Equals Net Treasury Account Deposits: $878

M/A/M 2011 Deficit: $264B for the quarter

So YoY for the 3 months ended May, the fiscal deficit has decreased by $103B (367B to 264B), due to a increase in deposits (either tax receipts, or perhaps the Fed refunding it's outsized "profits" due to QE to Treasury this year), as net withdrawals (spending) are actually down, nominal, by $22B, YoY for these same 3 months.

Total loans and leases (TLL) in bank credit rose by $9B over this same 3 month time period this year to $6,725B, but at the end of May 2010, total loans and leases stood at $6,893B, so hard to tell what TLL did YoY for the 3 months ended May, but we at least can see that TLL have collapsed by $168B (that's baaaaad) YoY for the year ended May.

With TLL still contracting YoY, and total government spending down $22B, it looks like we are looking at a negative GDP number for these 3 months, unless net imports have decreased by a greater amount.

This is pretty bad when the best thing we can look forward to is a hope that we imported less to get us some US GDP "growth".

Friday, June 24, 2011

Breakout of BEA's 1st Q 2011 GDP Report by Sector

Consumer Metrics Institute: The BEA's Third (and "Final") Estimate of First Quarter 2011 GDP

Summary:

The Bureau of Economic Analysis (BEA) revised their estimate of the annualized growth rate of the first quarter 2011 U.S. Gross Domestic Product (GDP) up slightly to 1.92%. This is their third and final regularly scheduled estimate of the first quarter's growth rate, although sweeping revisions of prior estimates can occur at the end of each July.

Don't Cry For Argentina

Some good:

Notably, the one creditor that was paid back in full — in 2006 — was the International Monetary Fund, to which Argentina owed $9.8 billion dating to the 1990s.A lesson for Greece is “whereas the commercial creditors are expected to take a haircut, the official creditors like the I.M.F. are not willing to,” said Robert S. Koenigsberger, chief investment officer with Gramercy, an emerging markets investment manager.“That is how commercial creditors get subordinated and bear the brunt of these failed bailouts,” Mr. Koenigsberger said.Since paying off the International Monetary Fund, Argentina has not borrowed from the fund. That has enabled the Kirchner governments to avoid the agency’s typical prescription of cutting state spending.[emphasis added]

Some bad:

For one thing, a decade later, Argentina has still not been able to re-enter the global credit market.“A default is not free,” said Jaime Abut, a business consultant in Rosario, a city north of Buenos Aires. “You have to pay the consequences, and for a long time. Argentina is no longer considered a serious country.[emphasis added]

Krugman responds: Don't Cry for Argentina

I was really struck by the person who said that Argentina is no longer considered a serious country; shouldn’t that be a Serious country? And in Argentina, as elsewhere, being Serious was a disaster.

Bill Mitchell elaborates on Argentina in Defaulting on public debt as a way to progress (September 7, 2010). Scroll down to Case study: Argentina 2001-2002 …

Bill concludes:

To reiterate, none of this discussion applies to truly sovereign nations who never face any solvency risk.I think the best thing a non-sovereign government can do in terms of advancing the interests of its people is to move towards sovereignty as soon as possible. That might involve jettisoning a currency arrangement (such as in Latvia, for example).It might require exiting a monetary union that has taken the currency-issuing monopoly away (such as the EMU nations). In this instance, that might necessitate a formal default on all debt that was incurred in the currency that the nation is exiting (such as Greece at present).The reality is that a sovereign government holds all the cards in this situation. Please read my blog – Why pander to financial markets– for more discussion on this point.There would be short-term costs but by re-establishing the currency sovereignty the nation will always be able to advance the best interests of its domestic economy.This doesn’t mean that a nation that is short of real resources etc will be able to establish a high material standard of living by moving to sovereignty. The real standard of living is always determined by the access a nation has to real resources. Fiscal policy does not create these resources but can ensure they are more fully utilised and thus more effectively deployed. A poor nation will not become rich just because it is sovereign.

Thursday, June 23, 2011

BEA: It's Not Borrowing, It's Double Entry Accounting

I've been doing some "lite" reading lately on the US International Transactions Accounts (ITAs), trying to increase my understanding of how the Commerce Department's Bureau of Economic Analysis (BEA) compiles their reports that document these cross-border economic flows.

So there you have it, right from the US Government official source of all the data that is the subject of all the "controversy". Let me repeat: "For each credit entry there MUST be an equal and offsetting debit entry (I hope you saw the word "must" and know what it means).

I found an interesting document at the BEA website that is a good top level overview of these reports. You can access the .pdf file here.

These BEA ITA reports cover the US balance of trade in the Current Account, as well as foreign purchases of US financial assets (such as Treasury Securities) in the Financial Account.

Fear mongers tell us often that (cue 'The Prospector') "We're borrowin' from the Chinese!", where we in the MMT paradigm would say rather that the Chinese are simply purchasing USD financial assets with the USD balances they accrue due to their outsized trade surplus with the US.

Who is right? Perhaps we should go to a neutral party to rule on this disagreement? Would the US BEA, the official government agency that maintains the records of these transactions qualify as an objective, unbiased authority on this topic? I would say so.

Then here is an excerpt from the BEA document I linked to above:

The ITAs apply a double-entry system of accounting in recording transactions: for any entry there must be counterpart entry. Exports of goods and services, income receipts, unilateral transfers to the United States, capital account receipts, decreases in U.S. assets abroad, and increases in foreign-owned liabilities in the United States are shown as credits (with a positive sign). Imports of goods and services, income payments, unilateral transfers from the United States, capital account payments, increases in U.S. assets abroad, and decreases in foreign owned liabilities in the United States are shown as debits (with a negative sign). For each credit entry there must be an equal and offsetting debit entry, and vice versa. For example, if a foreign resident purchased a U.S. good with a check drawn against its U.S. bank account, the offset to the credit entry for U.S. goods exports would be a debit entry for foreign-owned bank-reported liabilities, reflecting the reduction in foreign-owned assets in the United States

So here is the "T-account" breakdown according to the BEA; Chinese trade surplus: DEBIT, corresponding increase in Chinese owned US liabilities: CREDIT. That's all folks. There is no "borrowing" or "lending" involved here.

These are not my opinions, or Mike's opinions, or Tom's or John's or Kevin's opinions; or any of the MMT thought leader's opinions. This is a statement of fact promulgated by the US BEA.

Someone needs to tell former tax collector extraordinaire Rep. Michele "Hu's Your Daddy?" Bachmann that the official US government agency in charge of maintaining the accounting for international transactions, (btw an agency that she approves the operating budget for via Congressional appropriation) disagrees with her moron description of international accounting transactions.

Eric Cantor announces he is introducing a balanced budget amendment

House Majority Leader Eric Cantor (R-VA) today issued the following statement regarding House consideration of a balanced budget amendment, H.J. Res. 1, sponsored by Congressman Bob Goodlatte:

“We are being asked by the Obama Administration to approve a debt limit increase. While President Obama inherited a bad economy, his overspending and failure to enact pro-growth policies have made it worse and now our national debt is currently more than $14 trillion. House Republicans have made clear that we will not agree to raise the debt limit without real spending cuts and binding budget process reforms to ensure that we don’t continue to max out the credit card. One option to ensure that we begin to get our fiscal house in order is a balanced budget amendment to the Constitution, and I expect to schedule such a measure for the House to consider during the week of July 25th. I have no doubt that my Republican colleagues will overwhelmingly support this common sense measure and I urge Democrats to as well in order to get our fiscal house in order."

(h/t Zero Hedge)

UPDATE: Oh, wait! It gets even crazier. Again, from ZH:

Bad News for Nuclear Power

Well-known physicist Michio Kaku just confirmed all of the above in a CNN interview:In the last two weeks, everything we knew about that accident has been turned upside down. We were told three partial melt downs, don’t worry about it. Now we know it was 100 percent core melt in all three reactors. Radiation minimal that was released. Now we know it was comparable to radiation at Chernobyl.***We knew it was much more severe than they were saying, because radiation was coming out left and right. So in other words, they lied to us.***In New York City, you can actually see it in the milk. You can actually see it has iodine, 131, actually spiked a little bit in our milk in New York City, but it is very small.

See also Nebraska Nuclear Meltdown? Coverage of Fort Calhoun and Cooper Nuke Power Plant Flooding on the Missouri River for updates from various local sources.

Meanwhile, Germany has announced intentions to phase out nuclear power over 11 years.

Almost three-quarters of Japanese favor nuclear phase-out.

MMT holds that the only actual economic constraint is real resource availability. Nuclear energy has been expected to be a principle contributor to future energy resources with the projected phase-out of carbon-based fuels.

Wednesday, June 22, 2011

Stephen Gordon: What A Balance Sheet Recession Looks Like

Stephen Gordon at Worthwhile Canadian Initiative has some charts up illustrating the balance sheet recession.

Nick concludes with:

"The US data go back to 1952, so I was able to check the last time the real, per capita value of US housing equity was at its current level. Even after looking at all of these graphs, the answer astonished me: 1978. Nineteen seventy-freaking-eight."And it isn't over yet.

Tuesday, June 21, 2011

"The protests in Greece concern all of you directly."

"I have never been more desperate to explain and more hopeful for your understanding of any single fact than this: The protests in Greece concern all of you directly."What is going on in Athens at the moment is resistance against an invasion; an invasion as brutal as that against Poland in 1939. The invading army wears suits instead of uniforms and holds laptops instead of guns, but make no mistake – the attack on our sovereignty is as violent and thorough. Private wealth interests are dictating policy to a sovereign nation, which is expressly and directly against its national interest. Ignore it at your peril. Say to yourselves, if you wish, that perhaps it will stop there. That perhaps the bailiffs will not go after the Portugal and Ireland next. And then Spain and the UK. But it is already beginning to happen. This is why you cannot afford to ignore these events."

Read the rest at Sturdy Blog, Democracy vs Mythology: The Battle in Syntagma Square

By Alex Andreou, a successful lawyer turned actor living in London.

The post ends with:

"Nassim Nicholas Taleb is the Lebanese-American philosopher who formulated the theory of “Black Swan Events” – unpredictable, unforeseen events which have a huge impact and can only be explained afterwards. Last week, on Newsnight, he was asked by Jeremy Paxman whether the people taking to the streets in Athens was a Black Swan Event. He replied: “No. The real Black Swan Event is that people are not rioting against the banks in London and New York."(h/t Yves Smith of Naked Capitalism)

Edward Harrison Clears Up An Apparent Contradiction By Bill Gross

Edward Harrison of Credit Writedowns has an explanation for Bill Gross's seemingly contradictory views about the need to reduce the deficit and his call for instituting a job guarantee, which would increase the deficit — and Ed credits MMTer Marshall Auerback for it. BTW, Marshal is a consultant to PIMCO, so it is possible that he is the source of Gross's position.

Jobs have to come first. We are already seeing cyclical unemployment turn into structural unemployment – and that permanently lowers output and increases deficits. [MMT economist] Stephanie Kelton is right when she says that “as long as unemployment remains high, the deficit will remain high.”

When the private sector is not willing or able to step up to the plate, then government has to.

Ed points out that, moreover, just increasing aggregate demand through stimulus is generally politically co-opted, channeling the stimulus to the influential rather than toward creating effective demand.

Trader's Crucible pointed out in a recent post that MMT economist Pavlina Tcherneva observed:

“As already noted, for Keynes, the principal goal of fiscal policy was to secure true full employment and the principle measure for adjudicating among different policy responses was their employment-creation effects (Kregel 2008). Unfortunately, what is considered to be Keynesian policy today is largely a misinterpretation of the Keynesian prescriptions, which largely stems from a fundamental misidentification of Keynes’s theory of effective demand with the theory of aggregate demand (Tcherneva 2011). In the General Theory, Keynes carefully articulated that employment determination depended not on the volume of aggregate demand but on the point of effective demand which was very hard to stabilize and fix at full employment.”(emphasis added)

Alex Andreou on Greece

Good write up by an Alex Andreou that was cross posted at Naked Capitalism on the current economic injustice and needless social stress that is being inflicted on the citizens of Greece. Link to the post at NC here: "Democracy vs. Mythology". He includes some empirical economic data that may dispel some of the propaganda and stereotyping that has been perpetuated by the MSM about the economy of Greece being "sub-par".

Right on Alex! This guy gets it, let's hope his wisdom is contagious.

Excerpt that is quite in paradigm:

Money is a commodity, invented to help people by facilitating transactions. It is not wealth in itself. Wealth is natural resources, water, food, land, education, skill, spirit, ingenuity, art. In those terms, the people of Greece are no poorer than they were two years ago. Neither are the people of Spain or Ireland or the UK. And yet, we are all being put through various levels of suffering, in order for numbers (representing money which never existed) to be transferred from one column of a spreadsheet to another.

Right on Alex! This guy gets it, let's hope his wisdom is contagious.

Monday, June 20, 2011

Edward Harrison sums up QE1, QE2, and QE3

Edward Harrison of Credit Writedowns explains QE1, QE2, and QE3 from the Fed's announced perspective and his own views, which is consistent with MMT.

What are the differences between, QE1, QE2, and QE3?

Ed thinks that should QE3 come, it will be after the Fed has firmly established the the overnight rate at zero, when it will shape the yield curve by setting price rather than quantity, reversing the strategy of QE2.

If this happens it will be completely in line with MMT's position that the government controls interest rates as it chooses, and the natural rate of interest (overnight rate) is zero.

While this is admittedly an emergency measure, it demonstrates what MMT has been claiming as a feature of the federal government's monopoly power as issuer of a nonconvertible floating rate currency.

Robert Reich on Marriner Eccles

Truthout posted an excerpt from Robert Reich's new book, Aftershock. It tells the story of Marriner Eccles, chairman of the Fed Marriner Eccles, who served in that capacity from November 1934 until April 1948. If you are not familiar with the story, it's a good, short read.

Others had advised reducing the national debt and balancing the federal budget, but Eccles had different advice. Anticipating what British economist John Maynard Keynes would counsel three years later in his famous General Theory of Employment, Interest and Money, Eccles told the senators that the government had to go deeper into debt in order to offset the lack of spending by consumers and businesses. Eccles went further. He advised the senators on ways to get more money into the hands of the beleaguered middle class. He offered a precise program designed “to bring about, by Government action, an increase of purchasing power on the part of all the people.”

Eccles arrived at these ideas not by any temperamental or cultural affinity—he was, after all, a banker and of Scottish descent—but by logic and experience. He understood the economy from the ground up. He saw how average people responded to economic downturns, and how his customers reacted to the deep crisis at hand. He merely connected the dots.

Noah Smith on Libertarianism

The economics blog 'Noahopinion' has an interesting post on the U.S. strain of libertarianism:

Libertarianism and the Tamerlane Principle.

excerpt:

Libertarianism and the Tamerlane Principle.

excerpt:

"This is why modern American libertarianism is so very, very flawed. The ideology professes to value liberty above all else, but it ignores the dynamic aspect. There is liberty today, and there is liberty tomorrow. Sometimes violations of liberty today (such as an income tax) are necessary to protect the body politic from far, far, far more heinous violations of liberty tomorrow".

"Most libertarians recognize this, and freely admit that defense is an exception to the "small government" rule. But an army is not going to be a very effective Tamerlane repellant without a large GDP and advanced technology to back it up. And what modern American libertarians either fail to understand, or refuse to accept, is that public goods are essential for a high GDP."

Austrian School versus MMT

Austrian School advocate Robin Koerner attacks MMT in an article written for the Huffington Post.

"First of all, the system described by MMT, while real, is obviously utterly unconstitutional. Second, (as the MMTers admit), the supply of money in the private sector remains critically important as inflation is the monster that must not be unleashed (and the Austrians know all about that). Third, everyone other than the government still use fiat money in creating the economic dynamics of the nation in a way that the Austrians best understand. And fourth, and perhaps most importantly, government cannot merely spend money into the private sector without choosing where and how to spend it. And any such choice removes spending power from private citizens and redistributes it just as surely as in the days when the likes of Hayek and von Mises, two of the greatest thinkers in Austrian economics, were doing their best work. Put simply, while MMT offers extraordinary insights into aggregates, no economic decision ever affects only an aggregate".

"First of all, the system described by MMT, while real, is obviously utterly unconstitutional. Second, (as the MMTers admit), the supply of money in the private sector remains critically important as inflation is the monster that must not be unleashed (and the Austrians know all about that). Third, everyone other than the government still use fiat money in creating the economic dynamics of the nation in a way that the Austrians best understand. And fourth, and perhaps most importantly, government cannot merely spend money into the private sector without choosing where and how to spend it. And any such choice removes spending power from private citizens and redistributes it just as surely as in the days when the likes of Hayek and von Mises, two of the greatest thinkers in Austrian economics, were doing their best work. Put simply, while MMT offers extraordinary insights into aggregates, no economic decision ever affects only an aggregate".

Ron Paul's Four Promises

“First, I will veto any spending bills that contribute to an unbalanced budget."

(Memo to Rep. Paul: Please read Stephanie Kelton, What Happens When the Government Tightens its Belt and What Happens When the Government Tightens its Belt, Part II. Then follow up with Obama’s Implausible Dream: Cut the Deficit without Destroying Jobs)

“Second, I will veto any spending bill that contains funding for Planned Parenthood, facilities that perform abortion and all government family planning schemes. Like millions of Americans, I believe that innocent life deserves protection and I am deeply offended by abortion. It is unconscionable to me that fellow Pro-Life Americans are forced to fund abortion through their tax dollars."

(He thinks that federal taxes fund federal expenditure. Someone please send him Warren Mosler's The Seven Deadly Innocent Frauds of Economic Policy before he makes a greater fool of himself.)

“Third, I will direct my administration to cease any further implementation of ObamaCare."

(Go back to letting insurance companies practicing medicine by denying treatment one's doctor recommends? Exclude people with pre-existing conditions? And what about those cost savings that CBO estimates? Oh, right, consumers exist for business.)

“And fourth, I will on day one of my administration begin to repeal by Executive Order unconstitutional and burdensome regulations on American business. I will be the first President to shrink the size of the Federal Register. We must create a favorable regulatory environment for U.S. business. This cannot be stressed enough.”

(Someone please ask Rep. Paul to read some of the writings of Prof. William K. Black on control fraud. The False Dichotomy between Banking Honesty and a Sound Financial System is a good place to start.)

(h/t Zero Hedge)

Trader's Crucible on Bitcoin

TC also mentions the problem of uneven large spreads in different locations.

I suspect that these coins are not fungible, because my 9 year old son would be able to rip the faces off of these spreads. The bitcoin is probably closer to a fad than a real form of money.

Blather from Mather

Financial repression is any public policy that is designed to influence the market price of financing government debts, either through government bonds or the nation’s currency. Direct methods of repression include things like setting target interest rates, monetizing government debt or implementing interest rate caps. Indirect methods include polices designed to change the amount of debt or currency at a given price. Examples include requirements to hold minimum amounts of government debt on bank balance sheets or establishing minimum requirements for government bonds in pension funds.

Governments may take these steps to improve their ability to finance public debt and forestall more painful adjustment processes, though there can be other motives, and because these methods are less transparent, and thus less controversial, than direct tax hikes or spending cuts. Investors should be wary of financial repression because it is primarily a tool to redistribute wealth from creditors (citizens) to debtors (governments) to the detriment of creditors, fixed income investors and savers....

It is important to realize these methods as practiced are only partially effective and cannot go on forever, as advanced economies continue to add significantly to their public debts despite low financing costs. Some intensification of financial repression, fiscal austerity, or stronger growth must occur to lower the likelihood of a future debt crisis.

Scott A. Mather, PIMCO Economic Outlook, Game Change for Bond Investors?

Note:

1. "Governments practicing financial repression may be transferring wealth from creditors (citizens [bondholders]) to debtors (governments) to the detriment of creditors, fixed income investors and savers [rentiers]."

Bond holders are clearly upset by the prospect that QE3 (if it comes about) will target price instead of quantity, thereby capping interest rates. Fed bond purchases also transfer the interest on those securities to government, reducing the non-government net financial assets that would have accrued.

PIMCO is apparently concerned that Bernanke has figured out how to neuter the "bond vigilantes" by taking control of interest rates along the yield curve, a control that naturally falls to government as the currency monopolist.

2. "It is important to realize these methods as practiced are only partially effective and cannot go on forever, as advanced economies continue to add significantly to their public debts despite low financing costs. Some intensification of financial repression, fiscal austerity, or stronger growth must occur to lower the likelihood of a future debt crisis."

Mather does not seem to get that sovereign debt crisis is an oxymoron for countries like the US that are monopoly providers of a nonconvertible floating rate currency. This also accounts for the hissy fits that Bill Gross has recently been throwing.

Obviously, this will not "go on forever." It is an attempt to turn the economy around, although perhaps a misguided one, or else a hail mary pass since Congress refuses to act fiscally.

But it won't end because "it can't go on forever." The Fed already sets the overnight rate, and there is no contradiction in its setting the yield curve, too.

(h/t Zero Hedge)

"You don’t need a weatherman"

"You don’t need a weatherman

To know which way the wind blows"

Bob Dylan — Subterranean Homesick Blues

"Media reports often fail to connect recurring demonstrations in Greece and Spain with those in the Middle East and North Africa (Tunisia, Egypt, Syria, Yemen, Libya, Bahrain). After all, the MENA demonstrations are ostensibly about democracy, while European countries already have functioning electoral systems. Protestors in Greece and Spain are instead decrying austerity programs resulting from governmental efforts to rein in deficits and debt burdens.

"At the core, though, all of these uprisings are about the simultaneous failure of modern economics and modern politics—even though systems differ somewhat from country to country. People in all of the nations mentioned have one thing in common: crushed expectations. Economists and politicians have promised jobs and growth, but instead citizens are seeing spreading unemployment, rising food and energy prices, and increasing economic inequality. Nowhere are there realistic prospects for a political remedy to worsening economic conditions. Thus, while unrest seems destined to spread and intensify in the months and years ahead, it has no clear long-term strategy or goal..."

Richard Heinberg makes the case in Energy Bulletin, Post Carbon Insitute that this is not only a financial crisis, but also a long-term problem involving real resources, especially, dwindling sources of abundant cheap energy that fueled extraordinary economic development in contemporary times.

Read the rest at Global Youth Uprising: Dashed Hopes, Anger, and Realism.

Germany is the problem, not Greece

Edmund Conway at The Telegraph makes a case that "Germany - not Greece - has 'destabilised the euro area and is one of the biggest road-blocks to its ultimate recovery" in Why Germany must exit the euro.

I agree, although admittedly this may be confirmation bias on my part. By way of disclosure, I have been saying for some time that the problem is Germany and have predicted that Germany will be forced to exit the euro first for political reasons, namely, voters are unlikely to approve the required transfers that only Germany can make in the absence of a fiscal union in addition to the existing monetary one.

The problem is the strength of the core, particularly Germany, rather than the weakness of the periphery. Germany's export economy has colonized the periphery and left them without the means to meet their financial obligations to the core's financial sector, which, according to neoliberal thinking, must be protected above all else as the source and allocator of capital. This ends by forcing austerity on the periphery, resulting in social unrest in the absence of a bailout, which Germans consider inflationary if monetary and unfair to them if fiscal. This obviously is not working, and no permanent fix is in sight. Bandaids are not doing it, either.

The EMU suffers from poor design, along with a fact that should have been obvious from the outset — Europe is not an optimal currency zone. Regardless of this, the Europeanizers pushed ahead with a plan that did not contain contingency planning for imbalances resulting in distortions and ultimately crisis.

See Bill Mitchell, Doomed from the start

If Germany exited, then the Deutschmark would be properly valued in the market immediately and the euro would fall. Now, the euro is undervalued wrt Germany, favoring Germany's export economy, while being overvalued wrt to the periphery, disadvantaging much of the rest of Europe, especially chronic net importers. It is already being said openly that what Germany attempted and failed at in WWII, it is accomplishing financially and economically through Eurozone asymmetry.

If the EZ is to work as a currency zone, then either a fiscal union must be established allowing transfers, or else the design must be revisited taking into consideration an optimal currency area. Presently, the economic disparity is creating too great an asymmetry.

UPDATE: Bill Black, It Became Necessary to Destroy the Periphery in Order to Save the Core’s Banks

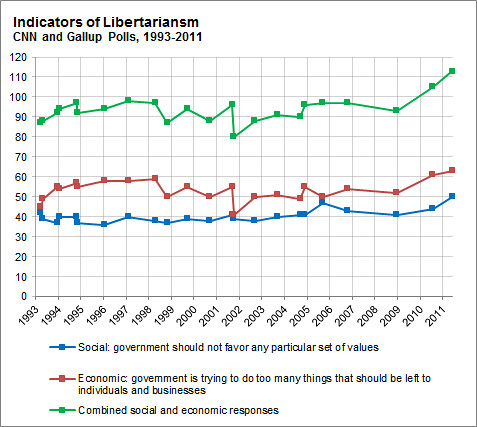

Libertarianism On The Rise

Über-statistician Nate Silver notes that according to recent polling, libertarian views are on the rise, both social libertarian and economic libertarian.

As a libertarian of the left this is welcome news to me. But as someone who understands the basics of MMT, along with the scientifically established fact that human beings are primarily social rather than individualistic, it is not all good news.

It is good news in that the country is moving past the days when culture was largely dictated by mores of the past. On the positive side for all libertarians, that is, of both left and right, this means that broader freedom and fundamental human rights are being recognized to a greater degree. We don't need politicians in our bedrooms, or government in the doctor's office when we visit.

On the negative side for those who understand MMT, the economic data may suggest a failure to comprehend sectoral balances and how government and non-government cannot be in surplus simultaneously. (See Stephanie Kelton, What Happens When the Government Tightens its Belt? and What Happens When the Government Tightens its Belt? (Part II) for the MMT reasoning.)

Ignorance of sectoral balances inevitably leads to policy choices that result in economic contraction and loss of financial independence for many as they are forced to draw down savings, sell assets, or borrow to maintain lifestyle, which is unsustainable. Those in the most precarious postion begin to fall into poverty — the opposite of libertarian values.

Read Nate's post at the New York Times (subscription required, but you can get in with this link)

Randy Wray On How Data Bears Out MMT

The post, The Austrian School responds to Dr. Galbraith, generated a lively debate and 174 comments. Some of those critical comments requested mathematical and empirical proof of MMT views.

UMKC Prof. Randy Wray just posted an overview of his earlier (2002) prediction about what developed into the GFC based on the sectoral balance approach and US data. In it, Randy gives the math — sectoral balances summing to zero — and the empirics — the data for the periods — to show how the MMT view bears out.

Randy also points out that the WSJ got it completely backwards at the time, and the mainstream still hasn't figured it out. Now, mainstream economists in the US, UK, and EZ are calling for "expansionary fiscal austerity" based on the same failed ideas, while MMT shows why this will lead to contraction instead.

Friday, June 17, 2011

Social Money

THE ties that bind the 92,000 residents of Macon, Georgia, are a little tighter these days. Since October, the locals - college students and senior citizens alike - have been playing Macon Money, a "social impact game" that uses a currency of the same name to overcome socioeconomic barriers in the small city by encouraging people from all backgrounds to meet and collaborate....

In the game, players receive "bonds", which are imprinted with Macon-inspired icons and symbols, such as peaches, guitars and butterflies. They can then redeem these bonds for notes of Macon Money, imprinted with the face of the town's most famous son, the late soul singer Otis Redding. These notes can be spent at participating local businesses, which the game's organisers reimburse with US dollars.

But there's a twist. Each person receives just half a bond and must locate the person with the other half - identified by its matching symbols - in order to redeem it. Often turning to social media such as Facebook and Twitter, matching players then meet in person to redeem the bond and get their Macon Money. The bonds range in value from $10 to $100....

Read the whole thing at New Scientist: Future of money: A currency that's building community

(h/t Senexx)

Thursday, June 16, 2011

Michael Hudson — Free Money for Wall Street, Bupkis for Main Street

In the case of bailing out Wall Street – and thereby the wealthiest 1% of Americans – while saying there is no money for Social Security, Medicare or long-term public social spending and infrastructure investment, the beneficiaries are obvious. So are the losers. High finance means low wages, low employment, low industry and a shrinking economy under conditions where policy planning is centralized in hands of Wall Street and its political nominees rather than in more objective administrators.

Michael Hudson mentions MMT in this post, although he is out of paradigm when he speaks of losses being born by taxpayers or Treasury bonds paid out of future revenues.

Most scathing in this acerbic critique is his showing how Michelle Bachman gets the truth of the bailout, whereas the political class either doesn't or is returning the favor to big donors in the financial sector.

"Because we think we may be the next Greece, we are turning ourselves into the next Japan."

Tim Duy at Fed Watch:

Bottom Line: Both monetary and fiscal policy suffer from the same impediment – the numbers needed to be effective, in both the size of the Fed’ balance sheet and the magnitude of the federal deficit, are so big that policymakers view them as potentially destabilizing, while the magnitude to which they might be willing to commit would leave them open to criticism that their policies are failures. The obvious fallback position is to embrace the devil you know, which in this case is an economy simply limping along.

Warren Mosler:

Because we think we may be the next Greece, we are turning ourselves into the next Japan.

Wednesday, June 15, 2011

Obama presides over the greatest wealth transfer to the top of any president in history!

Obama promised to help working people. Instead, he has presided over the greatest wealth transfer to the top of any president in history. Look at what has happened to workers's share of national income since he took office.

How to counter the, "printing money" line when explaining MMT

I was talking to Warren Mosler yesterday and he came up with a good way (I thought) of countering the "printing money" line that we often hear.

"All government spending is printing money. And all taxation and spending reductions are 'un-printing' money."

Quick, concise, clever.

Feel free to use it.

Tuesday, June 14, 2011

Bernanke finally gets it that the Fed controls the yield curve?

Edward Harrison of Credit Writedowns:

This time the Fed will target price instead of quantity.

MMT economists were saying from the beginning that this is what the Fed would have done to control the yield curve. Now Bernanke seem to have figured out that he should be targeting price (yield) instead of quantity (announcing the total projected buy).

Harrison sums up what is likely to happen very well including this important quote of Bernanke:

So what then might the Fed do if its target interest rate, the overnight federal funds rate, fell to zero? One relatively straightforward extension of current procedures would be to try to stimulate spending by lowering rates further out along the Treasury term structure–that is, rates on government bonds of longer maturities. There are at least two ways of bringing down longer-term rates, which are complementary and could be employed separately or in combination. One approach, similar to an action taken in the past couple of years by the Bank of Japan, would be for the Fed to commit to holding the overnight rate at zero for some specified period. Because long-term interest rates represent averages of current and expected future short-term rates, plus a term premium, a commitment to keep short-term rates at zero for some time–if it were credible–would induce a decline in longer-term rates. A more direct method, which I personally prefer, would be for the Fed to begin announcing explicit ceilings for yields on longer-maturity Treasury debt(say, bonds maturing within the next two years). The Fed could enforce these interest-rate ceilings by committing to make unlimited purchases of securities up to two years from maturity at prices consistent with the targeted yields. If this program were successful, not only would yields on medium-term Treasury securities fall, but (because of links operating through expectations of future interest rates) yields on longer-term public and private debt (such as mortgages) would likely fall as well.

There's much more in Harrison's summary, including a quote from Scott Fullwiler. However, I disagree with Ed about the outcome, which he thinks will result malinvestment. (Ed is an Austrian economist.)

Subscribe to:

Posts (Atom)